Inflation can impact our finances in a number of ways – from the cost of our weekly shop to the value of our long-term savings – but what exactly does it mean?

Inflation might be something that not many people understand. Yet, we all experience it and feel its effects. When you head to the store expecting to spend a budgeted amount of money on something, only to spend a lot more, you’ve experienced inflation. Of course, when a price rises on a product it’s not always due to inflation. Yet, inflation still affects your cost of living by increasing the cost of goods and services.

This is why it’s so important to consider inflation when planning for the future, even if the future is as soon as next year. Especially when planning for retirement, you need to ask yourself what you want as your standard of living because inflation directly affects your lifestyle.

Therefore, it’s important to understand how inflation works, as well as the effects it could have on your financial planning.

What is Inflation? How does it personally affects you?

Inflation is often referred to as a “measure of the increase in the price of goods and services over time”.

Yes, it affects everyone. Yet, it affects everyone very differently. Your lifestyle is based on your income and your expenses. Sometimes, people who have a high standard of living but not a high enough income end up borrowing money to make up the difference.

Inflation not only affects the cost of living – things such as transport, electricity, and food – but it also impacts interest rates on savings accounts, the performance of companies, and in turn, share prices.

When inflation rises, borrowing money becomes very expensive. This means either people take out fewer loans or they’re unable to spend less money because it’s going towards debt payments. This reflects a reduction in the purchasing power of your money. In other words, this impacts your ‘buying power, as you’re now able to buy less with your money.

For those people whose standard of living matches their income, inflation can be both a positive and a negative. Usually, when inflation rises, your income also rises as there are adjustments based on the cost of living. However, even with an increased income, expenses also rise. For those on a fixed income – like retirees – inflation can greatly affect their standard of living.

Let me give you a few examples of where we were to where we are now when it comes to our spending habits or lifestyle expenses.

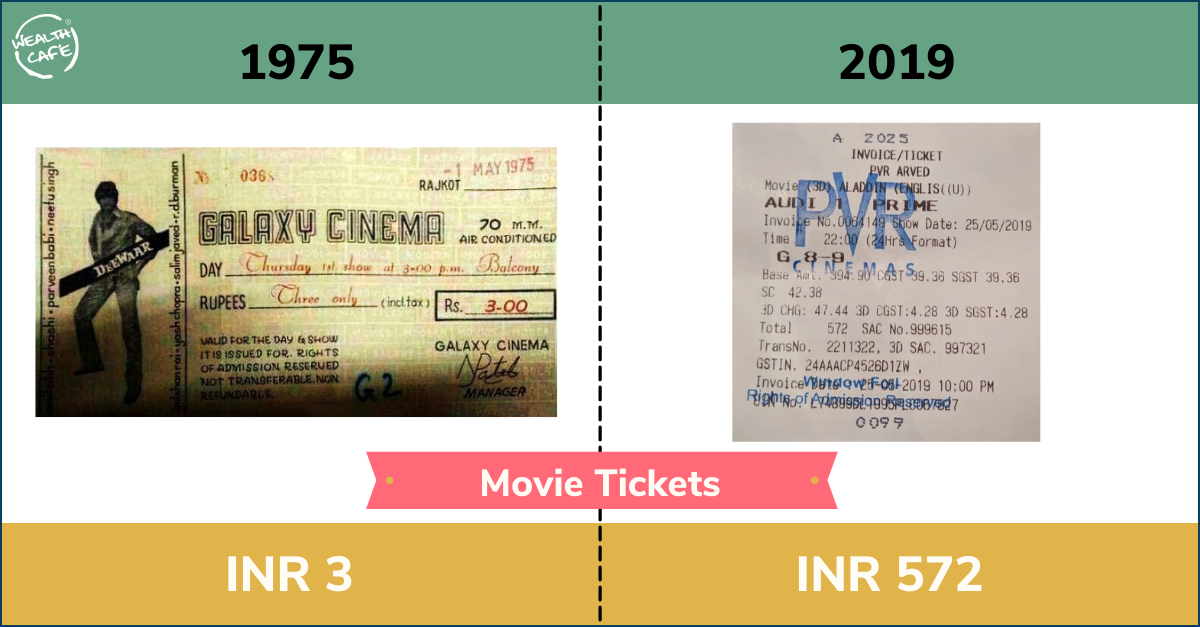

Movie tickets: From 1975 to 2015

Watching the latest flick, on opening day for just 3 rupees. Madness. Of course, while there are places where you can still get tickets for a tenner (DDLJ in Maratha Mandir), those places are few and far between.

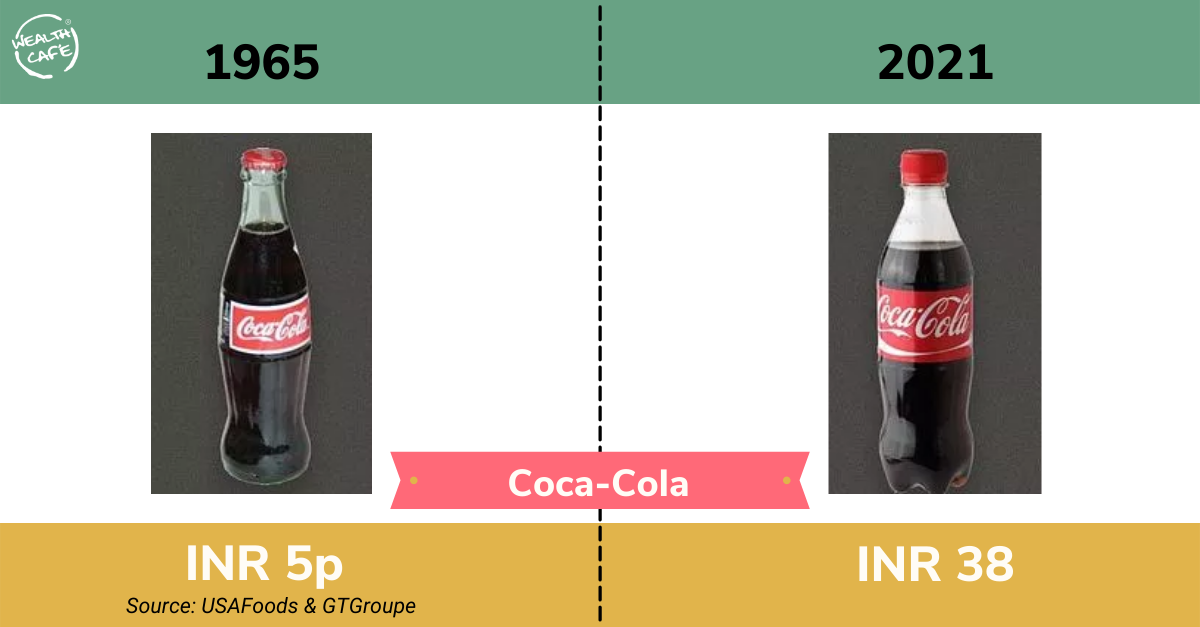

Coca-Cola: From 1965 to 2015

This was before Coca-Cola was kicked out of the country in 1973. And here we thought a small Coke for 5 rupees was a big deal.

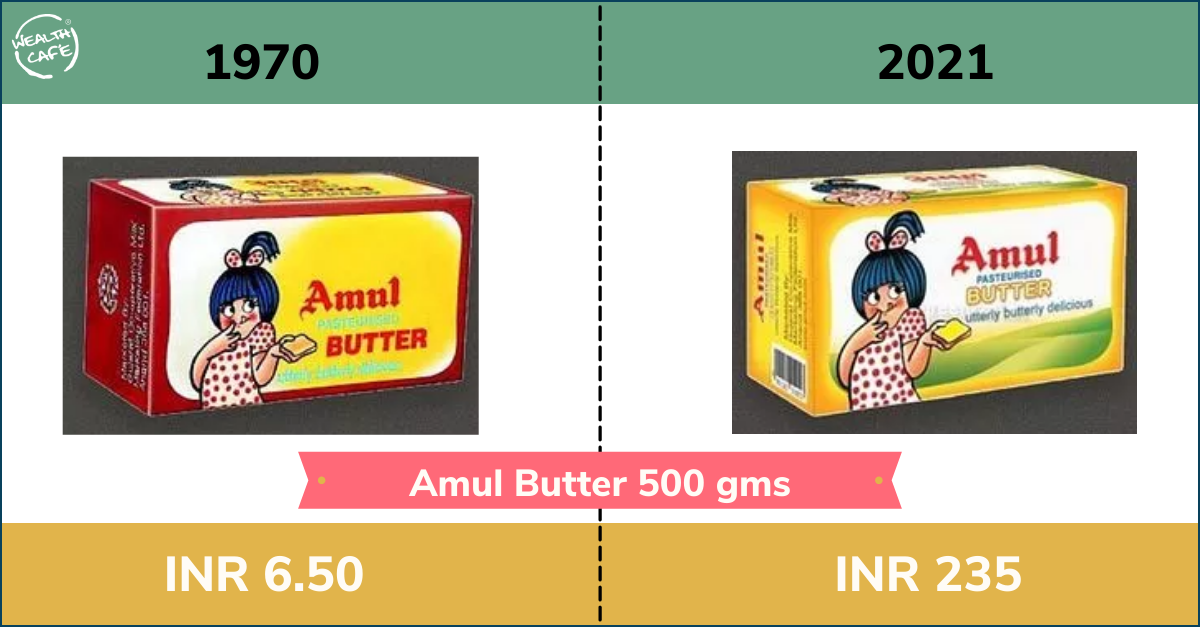

Amul Butter 500 gms: From 1970 to 2015

Guess those really were "butter" times, eh?

Is Inflation bad for everyone?

Inflation is perceived differently by everyone depending upon the kind of assets they possess. For someone with investments in real estate or stocked commodities, inflation means that the prices of their assets are set for a hike. Those who possess cash may be adversely affected by inflation as the value of their cash erodes. A higher rate of inflation can make repaying loans easier because they can end up paying back less money if the interest rate is lower than the rate of inflation.

Therefore, Inflation influences all aspects of life. You’re going to have to navigate a variety of risks now and in the years ahead, no matter which direction inflation swings. Since everybody relies on goods and services in one way or another, inflation is felt by everybody – either negatively or positively. The best thing to do is to plan for it. If you are saving for the future, pay attention to inflation.