Are you ready to embark on an exciting journey abroad? Whether you're seeking work opportunities, thrilling adventures, or new experiences, moving to a different country brings about a lot of changes. It's not just about adapting to a new culture and lifestyle; it also involves undergoing a financial transformation. One such crucial aspect that deserves your attention is your existing savings bank account.

When you become a Non-Resident Individual (NRI), it becomes necessary to update your current Savings Bank Account to an NRO (Non-Resident Ordinary) account. Furthermore, if you wish to send money from your earnings abroad to India, you'll need to open an NRE (Non-Resident External) account.

So, what exactly are NRO and NRE accounts? Let’s understand more about it in detail with the help of examples.

Non-Resident Ordinary (NRO) Account:

- An NRO account is designed for managing your Indian income and local transactions.

- It allows you to hold and manage income earned in India, such as rent, dividends, or pension.

- Your existing savings account in India can be converted into a NRO account or a new account can be opened with funds generated in India or through local sources.

- The money in an NRO account, including foreign currency deposited into it, is maintained in the Indian rupee.

- You need to pay taxes on interest earned from the NRO account. TDS on such interest is applicable at the rate of 30.9% (30% tax rate + education cess & surcharge if any)

- Compliance to remit funds from NRO - In order to remit funds from the NRO account, you would need to submit two documents: Form 15 CA and Form 15 CB. The purpose of both these documents is to ensure that taxes are collected on the funds before they are remitted abroad as it becomes difficult to recover taxes at a later stage.

Example: Suppose you own a property in India and earn rental income from it. In that case, you can have the tenants deposit the rent directly into your NRO account. You can then use the funds in this account to pay property-related expenses or meet other financial obligations in India.

Non-Resident External (NRE) Account:

- On the other hand, an NRE account allows you to hold and manage your foreign income in India.

- It is maintained in Indian Rupees (INR) and is freely repatriable, meaning you can transfer funds back to your foreign account without any restrictions.

- The account can be opened with funds earned from overseas or through foreign currency deposits.

- Interest earned on NRE accounts is exempt from Indian income tax.

- You can use the funds in your NRE account to make investments, pay bills, or meet any other financial obligations in India.

Example: Let's say you are working abroad and earning in a foreign currency. By opening an NRE account, you can seamlessly transfer your income to India, maintain a financial presence, and utilize the funds for various purposes such as investments into stocks, mutual funds, deposits, etc, or family expenses.

FREQUENTLY ASKED QUESTION

Q1. Why is it necessary to convert my bank account to an NRO account? Can I still continue with my existing bank account after I become an NRI?

Ans. According to FEMA regulations, it is mandatory to convert your existing savings account to an NRO account when your status changes to NRI. Holding a resident savings account as an NRI is illegal and can result in penalties of up to three times the amount involved or INR 2 Lakhs (when the sum cannot be quantified). A daily penalty of INR 5,000 will also be charged until the penalty is paid.

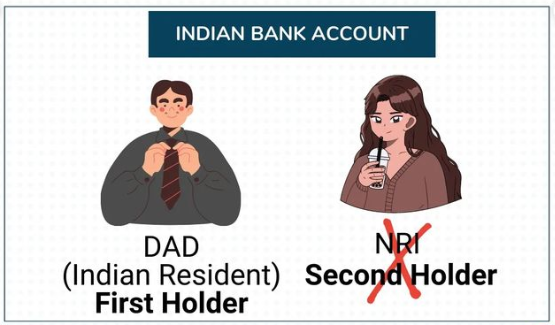

Q2. Can an NRI be a second holder of their relative's bank account?

Ans. No, it is not legally permitted for an NRI to hold a resident savings bank account, even as a second holder, once they become an NRI.

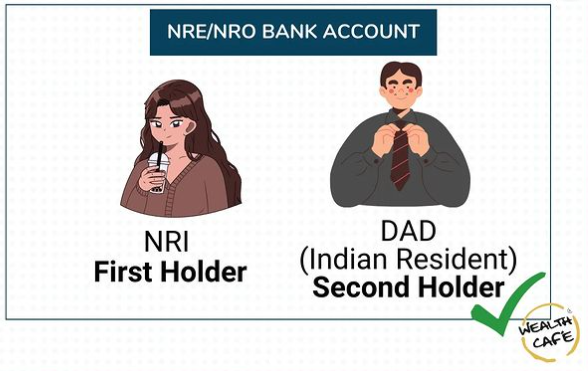

Q3. Can an Indian resident be a second holder of an NRI's NRO/NRE account?

Any Indian resident can be a holder of an NRI’s NRO account, whereas only an Indian resident relative can be a second holder in an NRE account.

Q4. Can an NRI transfer money from NRE A/c to their foreign country?

Ans. Yes, both the Principal amount and interest earned are freely and completely transferable without any limit.

Q5. Can an NRI transfer money from their NRO account to a foreign country?

Ans. Yes, funds can be transferred post payment of applicable taxes with a limit of USD 1 million in a financial year along with their other eligible assets.

Q6. Can an NRI invest in India using funds from their NRE/NRO accounts?

Ans. Yes, an NRI can invest from both, NRE and NRO accounts. While the NRE account is an external account and hence repatriable, the NRO account is a resident account and hence the funds are non-repatriable beyond the limit of $1 million per year.

Q7. What are the documents required to convert the existing account?

Ans. The following documents are required for the conversion process:

- FEMA declaration form

- Copy of PAN card

- Passport size photographs

- Foreign residence address

- Copy of work permit/valid visa/OCI or PIO card

- Copy of passport

Note: If any document is in a foreign language, it is important to provide a certified English-translated copy.

Q8. Is interest earned on NRE/NRO account taxable?

Ans. Interest earned in your NRE account is not taxable in India. However, Interest on the NRO account is taxable in India and will be liable for TDS. You can check Form 26AS for TDS deducted.

Q9. Can I claim a refund on TDS deducted from interest earned from the NRO account?

Ans. Yes, you can claim the refund of the TDS deducted on NRO interest income if your total income earned from or accrued in India is less than INR 2.5 Lakhs. You can claim a refund by filing Income Tax Return on Income Tax Portal.

I hope we have answered all your questions regarding NRE and NRO accounts. However, it is advisable to consult with your bank or a financial advisor to understand specific requirements, documentation, and any other applicable regulations based on your situation. If you have any queries, feel free to contact us at iplan@wealthcafe.in. We are SEBI - Registered Investment Advisors (RIA) and have been working with Non- Resident Individuals like you for over 14+ years now.