The tides may appear to have calmed down for now but we never know what is in store for us next. Some relaxations have definitely come out and some more are expected. However, this does not cure COVID 19, it just prepares us for the new normal of living with Covid as we begin to resume our old routines.

While there are many uncertainties looming over us, including pay cuts and job loss, some of you guys asked us if they should discontinue/pause their SIPs under these circumstances?

Like always my answer to this will depend upon how much extra cash you have left each month and if there is an Emergency Fund (equal to 4/6 months of your monthly expenses) in place to take care of these uncertain times.

- If you have not been affected by pay cuts, you must continue your SIPs as before. Additionally, since you are spending less than before, the savings again must get channeled into your investment portfolio.

- If your pay has been reduced, counter that with the reduced spends, and if your total savings are still the same, continue with your SIPs. If the savings are lower, then you can dip into your Emergency Fund to ensure your SIPs don't stop. If you have not set up an EMergency fund, then you will have to reduce your monthly SIP to match the amount you are able to save each month.

- If you have lost your job, or your salary has been paused, then you can fall back on your emergency fund to take care of your monthly expenses. SIPs will have to be stopped and will suffer.

What is the point of SIPs right now?

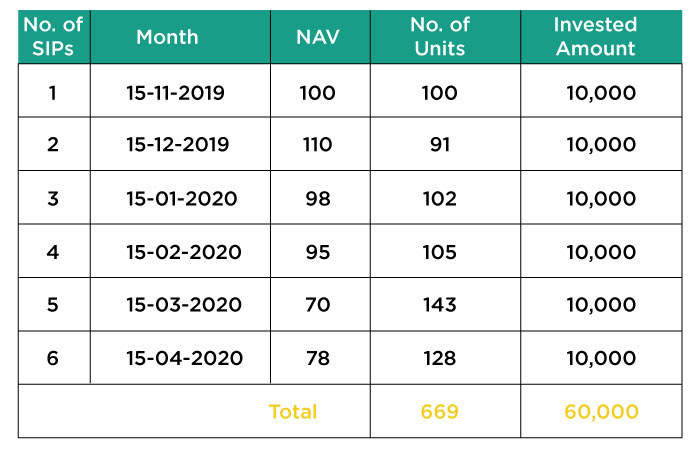

SIPs (known as systematic investment plans) are where you invest a fixed amount of money into a choice of your mutual fund at regular intervals (generally monthly). It is an automated process and the amount is debited from your bank and mutual fund units credited to you.

Buying in a falling market reduces your cost giving you higher benefits when the market goes up. To understand this better, let us run you through this example.

You get more units when the fund's NAV (market price) is lower

You get less units when the fund's NAV (market price) is higher.

As of 10 May, the NAV is priced at 85, hence the value of your investments will be 54,880 @5% loss.

Instead of doing SIP, had you invested a lump sum of INR 60,000 on 15 November, you would have got only 600 units (as opposed to 669 here) and the value of your investments would be INR 51,000 on 10 May 2020 (at a 15% loss).

No one knew that the market would fall so drastically and be so volatile in 2020, but your SIPs definitely help you to invest in a staggered and make most of the down market.

Everyone wants to know when we will reach the bottom to buy the maximum number of units. But it is anyone's guess when the markets will reach the bottom or what the bottom price is. Hence, SIP is your friend in such markets. When you continue your SIPS, your amount keeps buying a varied number of units (more in a down market) and thus, helping you to average your cost of buying.

Do not stop your SIPs now just because the markets are down, for all you know this time may turn out to be a bargain and help you get better returns in the future.

1.Always have an Emergency Fund (at least 4 times your monthly expenses) invested in risk-free investment options.

1.Always have an Emergency Fund (at least 4 times your monthly expenses) invested in risk-free investment options. 2.Have your Health Insurance and Life insurance in place.

2.Have your Health Insurance and Life insurance in place.

Investing Rule 101 - High Risk = High Returns & Low Risk = Low Returns

Investing Rule 101 - High Risk = High Returns & Low Risk = Low Returns