How to know your UAN?

a. Through Employer

In the normal course, you can easily get your Universal Account Number from your employer allotted to you by the EPFO. Some employers print the UAN number in the salary slips too.

b. Through UAN Portal using PF number/member ID

It is possible, that you are unable to get your Universal Account Number from the employer, you can obtain the UAN number through UAN portal also. You need to follow the below steps:

Step 1: Go the UAN Portal https://unifiedportal-mem.epfindia.gov.in/memberinterface/ Step 2: Click on the tab ‘Know your UAN Status’. The following page will appear.

Step 3: Select your state and EPFO office from dropdown menu and enter your PF number/member ID alongwith the other details such as name, date of birth, mobile no, captcha code . You can get the PF number/member ID from your salary slip. Enter the tab ‘Get Authorization Pin’.

Step 4: You will receive a PIN on your mobile number. Enter the PIN and click on ‘Validate OTP and get UAN’ button.

Step 5: Your Universal Account Number will be sent to your mobile number.

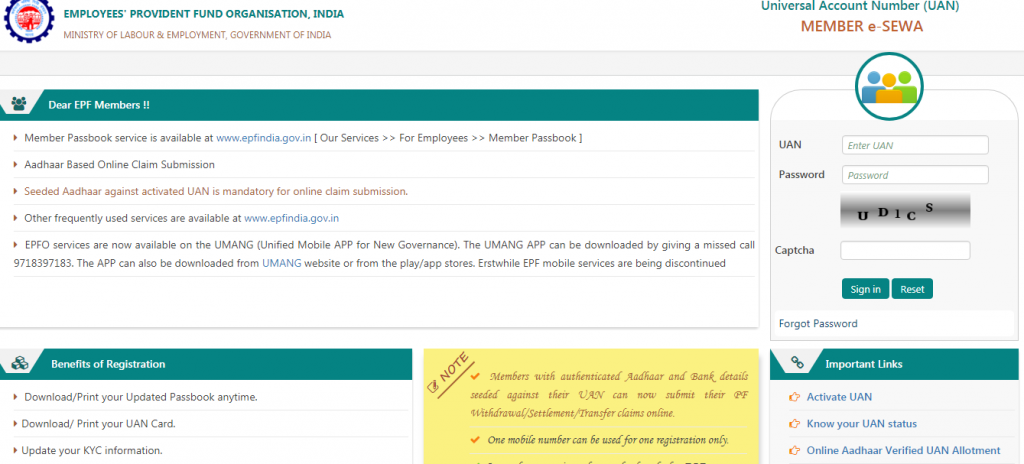

How to activate and login to the EPFO website using UAN?

In order to activate UAN, it is essential that you have your Universal Account Number and PF member id with you. Given below are steps to activate.

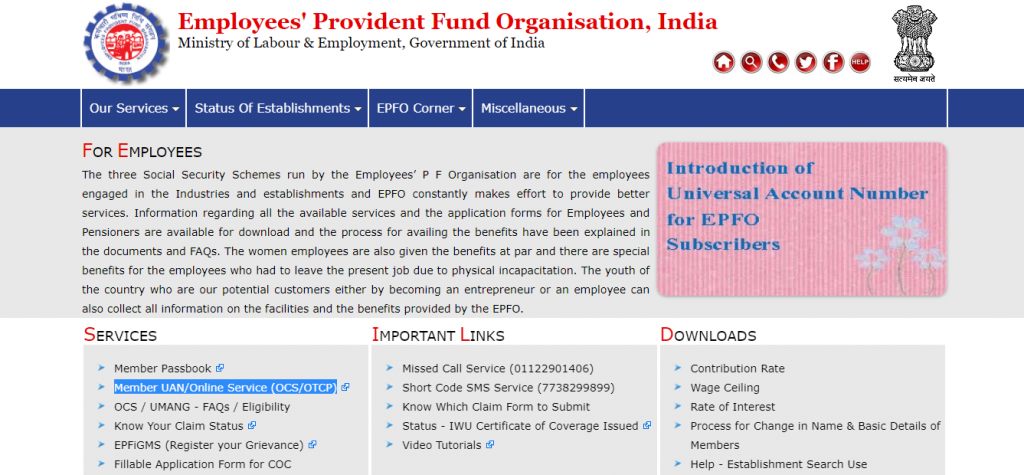

Step 1: Go the EPFO homepage and click on ‘For Employees’ under ‘Our Services’ on the dashboard.

.

Step 2: Click on ‘Member UAN/Online services’ in the services section. You would reach the UAN portal.

Step 3:

- Enter your Universal Account Number, mobile number and PF member ID. Enter the captcha characters. Click on ‘Get authorization PIN’ button. You will receive the PIN on your registered mobile number.

- Click on ‘I Agree’ under the Disclaimer checkbox and enter the OTP that you receive on your mobile number and click on ‘Validate OTP and Activate UAN’.

- On activation of the UAN, you will receive a password on your registered mobile number to access your account.

- If you wish to change your password it is possible, when you log into the UAN portal with your Universal Account Number as id and the password you receive on your mobile number.